Winery TTB Report Mistakes: 6 Common Filing Errors and How to Avoid Them, with Ann Reynolds, Owner of Wine Compliance Alliance

Ann Reynolds ran her first harvest in 1993. In 1998, she started doing winery compliance at Sterling Vineyards in Calistoga, working through questions that nobody around her could easily answer, piecing together an understanding of federal reporting that she largely had to build herself. That experience of looking for guidance that did not exist is what prompted her to start Wine Compliance Alliance in 2009, building the accessible, practical compliance training she had needed as a young winery professional and could not find.

She sat down with Lauren Heindel to walk through the six most common mistakes wineries make when filing the TTB 5120.17 Wine Premises Operations Report, covering what each error is, why it happens, and the specific steps that prevent it.

The TTB 5120.17 is one of the most consequential reports a winery files, and it is also one of the most commonly filed incorrectly. The mistakes are rarely intentional. They happen because the rules are specific and not obvious, because production records do not always reach the person doing the filing, and because many wineries are still using paper-based workflows that make errors harder to catch before they become a compliance problem.

In this episode, we cover:

Why the wrong person signing a TTB report is a compliance violation, and the two filing designations that establish who has authority

How to determine your required filing frequency using in-bond gallon totals and excise tax thresholds

When to file an amended report, and why leaving a known error uncorrected creates compounding problems in every report that follows

Why beginning on-hand inventory numbers must match exactly the ending numbers from the previous report

What it means when Line 2 (produced by fermentation) requires corresponding entries in Section 4 (materials received and used)

What an out-of-balance report is, how Pay.gov prevents it from happening, and how to resolve one when it does

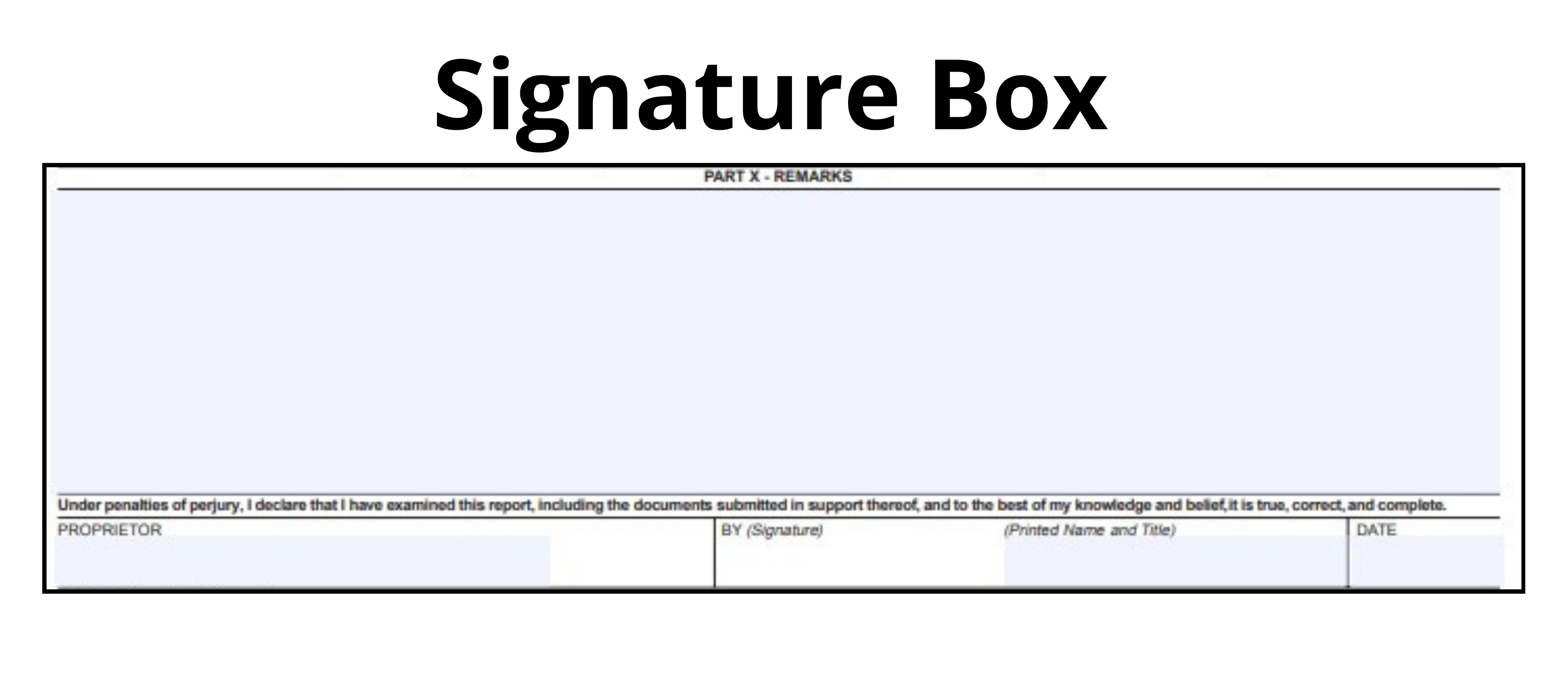

Mistake 1: The report is signed by someone without authority

The TTB requires that the person who signs and submits the 5120.17 report has an official designation on file with the agency. Two designations qualify: power of attorney and signing authority. Neither is automatic, and not every staff member holds one.

Power of attorney is filed with the TTB for a specific named individual. When that person leaves the winery, a new power of attorney needs to be filed before the next person can take over filing duties. Signing authority works differently: it is set up by job title rather than by name. If the signing authority designation was established for the title of winemaker, any person holding that title is covered, which means a winery does not need to file new paperwork every time there is turnover in the role.

Power of attorney is specific to individuals by name. Signing authority can be set up by title, president, winemaker. Things like that. Just as an FYI. A great designation.

Ann Reynolds , Owner

Wine Compliance Alliance

For wineries filing through Pay.gov, this mistake is structurally prevented. Pay.gov will not grant an account to anyone who does not already have power of attorney or signing authority on file with the TTB. That gatekeeping removes the possibility of an unauthorized signature at the platform level. The mistake only applies to wineries submitting paper forms with a wet signature, where no system check exists to flag the issue before the form is mailed.

Ann recommends that every winery have at least one person on staff who knows where the TTB entity file is and who currently holds power of attorney or signing authority. Staff changes happen, and when the person who was filing leaves, someone needs to know whether a new designation needs to be filed before the next report is due. This is a ten-minute review that becomes a much larger problem if it is skipped.

Mistake 2: Not filing as often as required

Most small wineries file their TTB report annually. Some of them are required to file more often and do not realize it. Filing frequency is determined by two metrics: the total gallons a winery holds in bond at any point during the calendar year, and the total federal excise taxes owed to the TTB.

For annual filing, both conditions must be met: the winery cannot exceed 20,000 gallons in bond at any point in the year, and cannot owe more than $1,000 in excise taxes. In-bond gallons includes both bulk wine (in tanks and barrels) and any bottled wine held at the facility before federal excise tax has been paid. For quarterly filing, the threshold rises to 60,000 gallons in bond with less than $50,000 in excise taxes owed. Any winery that holds more than 60,000 in-bond gallons at any point in the year is required to file monthly.

If you have more than 60,000 gallons of in-bond wine, then you would have to be filing the report monthly. But yeah, annually, quarterly, or monthly.

Ann Reynolds , Owner

Wine Compliance Alliance

The error typically happens when a winery grows or makes a large bulk wine purchase without revisiting its reporting obligation. A winery that qualified for annual filing in prior years may cross a threshold after a large harvest or acquisition without recognizing that a new obligation has been triggered. Ann notes that reviewing the in-bond gallon count at the time of filing, rather than assuming it matches the prior year, is the most direct way to stay on the right schedule.

Ann recommends checking your current in-bond gallon total before each filing, running through bulk wine in tanks and barrels plus any in-bond bottled wine on-site. If your total is close to a threshold, even briefly during the year, you should verify your filing frequency is still correct. Switching to a more frequent schedule is always permissible and is far less disruptive than an inquiry from the TTB after the fact.

Mistake 3: Not filing amended reports when records change

Wineries discover errors in previously filed reports regularly. A bottling that was not recorded before the report went out. A gallon count that was off because the cellar notes did not reach the person filing. An entry that was simply missed. These gaps are a normal part of production, and the TTB has a specific process for correcting them: the amended report.

The problem is that many wineries do not use it. They find the error, acknowledge it, and move on without going back to correct the filed record. This creates a continuity problem. Because each report’s beginning on-hand inventory must match the ending on-hand inventory from the prior report, an uncorrected error compounds through every subsequent filing. The gap stays open and accumulates until the winery eventually has to trace it back and resolve it, which is considerably harder six months or a year later.

If you've filed your report for November 2024, and then the winemaker or somebody from the cellar staff comes and informs you that you actually bottled this other wine, or the numbers that went into that report were wrong, for whatever reason, they were higher, they were lower. Which means you then have to go back in and file an amended report.

Ann Reynolds , Owner

Wine Compliance Alliance

Filing an amended report through Pay.gov requires finding the original filed report, clicking one button to open an amended version, correcting the entries, and saving it. The platform automatically marks it as an amended report. For wineries still filing on paper, the same correction requires starting the form over from the beginning, which is one of the stronger practical arguments for making the move to online filing.

Build a brief confirmation step into the workflow around bottling specifically. Before filing any report that covers a period with a bottling event, check in with whoever ran the run to confirm the gallon and case count. That single step, done in five minutes, prevents most of the scenarios that produce amended report situations in the first place.

Mistake 4: Beginning on-hand numbers that do not match the previous report

The TTB 5120.17 report is a continuous ledger, not a standalone document. Each report begins where the last one ended. The beginning on-hand inventory numbers on the current report must exactly match the ending on-hand inventory numbers from the prior report. When they do not, the TTB flags an inconsistency, and an amended report is usually needed to resolve it.

Ann describes the 5120.17 as functioning like a balance sheet: it has amounts that increase the inventory and amounts that decrease it, and the totals have to reconcile across the period. Because each report connects to the next one, a number that is off in one filing creates a gap that persists until it is corrected. This is another reason why filing amended reports when errors are discovered matters: leaving a discrepancy in a prior report eventually collides with the beginning numbers on a subsequent one.

Think about it like reading these reports like a book. They have to connect to each other. This report is basically a version of a balance sheet. The numbers have to connect from one report to the next.

Ann Reynolds , Owner

Wine Compliance Alliance

Ann’s recommendation for preventing this mistake is simple: whenever you sit down to file a new report, pull up the last filed report and keep it visible. Copy the ending on-hand inventory numbers directly onto the beginning lines of the new filing. Do not type from memory, do not estimate, and do not pull the number from a different source. If the records show a different figure than what was on the last report, that is a flag that an amendment may be needed before the new report is filed.

Pay.gov maintains a complete archive of every report your winery has filed through the platform. If you are not sure where your prior reports are or what the last ending inventory numbers were, they are accessible there whenever you need them. Having that archive available means you never have to guess at the beginning numbers for a new filing.

Mistake 5: Line 2 does not match Section 4 during harvest

This mistake is more technical than the others, but Ann identifies it as one of the most common sources of inaccurate reports. Line 2 of the 5120.17 is labeled “produced by fermentation,” where wineries record the gallons of wine created during the reporting period. Section 4 is labeled “materials received and used,” which is where wineries record incoming fruit and juice received at the facility. The two sections are directly connected: gallons appearing on Line 2 must have corresponding entries in Section 4 that account for the fruit or juice that became those gallons.

The confusion often comes from wineries believing they are double-counting when they enter the pounds of grapes received in Section 4 and then record the resulting gallons of wine on Line 2. Ann is clear that these are not duplicate entries. Section 4 captures what arrived at the winery in raw form. Line 2 captures what that material became after fermentation. They describe two different things at two different points in the same process, and both entries are required.

If a winery is listing gallons on line two produced by fermentation, then that means that they would've had to have received in some fruit, some pounds of grapes or whatever it might be. All of that information, either you're receiving in fruit or receiving in juice, those numbers first show up on this report in part four.

Ann Reynolds , Owner

Wine Compliance Alliance

Section 4 is only active during harvest. For months outside of harvest season, it will be empty, and that is correct. Ann notes that filing quarterly rather than annually makes this section easier to manage because the harvest-period entries appear in the specific quarter they belong to, rather than being absorbed into a year-end report that spans the entire winemaking cycle.

If your winery uses a production management platform, the tax class change entry is typically the step that generates the gallons that belong on Line 2 in platforms like InnoVint. Knowing which action in your production system feeds which line on the TTB report removes the ambiguity for the person responsible for the filing, particularly when that person is not the same one who ran the harvest.

Mistake 6: Submitting a report that is out of balance

The 5120.17 report has multiple sections, each of which functions as a mini balance sheet. Each section sums inflows and outflows, and the totals must match. When the math does not close, the report is out of balance. Pay.gov will not allow an out-of-balance report to be submitted: the platform highlights the mismatched lines before the filer can proceed, which makes this mistake structurally impossible for wineries filing online.

For wineries still using paper forms, the error can reach the TTB without being caught. And for wineries using Pay.gov who encounter an out-of-balance flag, the path to resolution requires finding the source of the discrepancy. The most common cause, in Ann’s experience, is gains and losses: a missed work order, an unrecorded loss, or an estimate that was slightly off creates a small gap that keeps the totals from reconciling.

Gains and losses is a common one that I see. The amounts can be off by one gallon or three gallons, a small amount, and they still don't match. I just simply go in and I massage the number to get it to the right math.

Ann Reynolds , Owner

Wine Compliance Alliance

Before adjusting gains or losses to close an imbalance, Ann recommends checking first whether a transaction was simply missing. A bulk wine receipt that was not recorded, a bottling run that did not make it into the production records, or a transfer that was overlooked can all create an out-of-balance condition that a missing entry would resolve without any estimation.

Ann is a proponent of filing quarterly even for wineries that qualify for annual filing, partly because of how much easier it is to trace and resolve imbalances when you are working with a three-month window rather than twelve. A gain or loss entry that went unrecorded in October is much easier to find and fix in late November than it is in the following spring when the year-end report comes due.

Watch or listen to the full episode on YouTube | Spotify | Apple Podcasts.

For more conversations like this, subscribe to Expert Talks and join The Punchdown, InnoVint’s online community for wine professionals.

Frequently Asked Questions about Filing TTB Reports for Wineries

What are the most common mistakes wineries make when filing TTB reports? +

The six most common mistakes when filing the TTB 5120.17 Wine Premises Operations Report are: having the report signed by someone without TTB power of attorney or signing authority on file, filing less frequently than required based on in-bond gallon totals and excise tax obligations, failing to file amended reports when prior reports contain errors, entering beginning on-hand inventory numbers that do not match the ending numbers from the previous report, listing gallons on Line 2 (produced by fermentation) without corresponding Section 4 entries for materials received, and submitting a report where section totals do not balance. Wineries using Pay.gov for online filing have the first and last mistakes prevented automatically by the platform.

How often does a winery need to file its TTB report? +

TTB filing frequency is determined by two factors: the total gallons held in bond at the winery at any point during the year, and the total excise taxes owed to the TTB. Wineries with fewer than 20,000 in-bond gallons and less than $1,000 in excise taxes owed qualify for annual filing. Wineries between 20,000 and 60,000 in-bond gallons and owing less than $50,000 in excise taxes must file quarterly. Wineries with more than 60,000 in-bond gallons at any point in the year are required to file monthly. These thresholds apply at any point during the calendar year, so a winery that crosses a threshold mid-year due to a large harvest or bulk purchase may need to adjust its filing frequency going forward.

What is the TTB 5120.17 Wine Premises Operations Report? +

The TTB 5120.17 is the Wine Premises Operations Report that all federally permitted wineries must file with the Alcohol and Tobacco Tax and Trade Bureau on a recurring schedule. The report tracks all wine held in bond at the facility during the reporting period, including inflows from production and purchases, outflows from bottling and sales, and beginning and ending on-hand inventory. It functions as a rolling balance sheet of wine held at the winery and is used by the TTB to calculate federal excise tax obligations. Filing frequency is annual, quarterly, or monthly depending on the winery's size and tax liability.

What is TTB signing authority, and how is it different from power of attorney? +

TTB power of attorney designates a specific named individual as authorized to file compliance reports on behalf of a permitted winery. It is individual-specific, which means it must be updated each time that person changes. TTB signing authority is a related designation that can be set up by job title rather than by name, covering anyone who holds that role at the winery without requiring a new filing when personnel change. Wineries filing through Pay.gov must have one of these designations established before accessing the platform, which prevents unauthorized individuals from filing reports.

When does a winery need to file an amended TTB report? +

A winery needs to file an amended TTB report any time it discovers that a previously filed report contains incorrect or incomplete information: a missing bottling event, incorrect gallon counts, a wrong beginning or ending inventory number, or any other entry that does not accurately reflect the period in question. Filing an amended report through Pay.gov is a straightforward process that flags the report as amended in the official record. Leaving a known error uncorrected creates a continuity problem because the beginning inventory numbers on the next report must exactly match the ending numbers from the prior one.